LESSON 5

Types of industries

1. Rooted industries

Refers to industries set up a specific area due to the existence of locational factors (such as market, raw materials, developed infrastructure among others). For example, a cement industry near the raw material source, a soft drink industry near a water body.

2. Footloose industries

Refers to industries that are not tied to any location and can therefore be located anywhere in response to any changing economic conditions. It is result of purely random selection and most small scale/ cottage industries are footloose in nature.

3. Tied industries.

Refers to industries located near the market of finished goods. This is because the final products are in most cases bulky or perishable.

4. Bulk gaining/weight increasing industries

Refers to industries located near the market because the finished products become bulky. For example, ship building industries.

5. Bulk reducing industries

Refers to industries located at the source of bulky raw materials to reduce the costs of transportation. This is because the finished products are less bulky.

Production/Planning period of a firm

[Firms use it when making decisions. Planning periods do not refer to a specific period of time (e.g. 2 months or 1 year), but depends on what the firm is able to do within that time. The short run of one firm may be the long run of another].

1. Market period (momentary period/ very short run)

This is a period which is too short for a firm to change its market supply and this period follows immediately after a price change. (If there is a change in price), the supply is perfectly inelastic that is, the firm is not able to vary output.

2. Short run

This is a period during which a firm can vary output by varying the quantities of variable factors but not the fixed factors. The firm can vary raw materials, labour etc while other factors like rent remain fixed. [Supply is price inelastic]

3. Long run

This is a period during which a firm varies its output by varying the quantities of all the factors of production but cannot change the state of technology. (Supply is price elastic).

4. Very long run (secular period)

This is a period that is so long that all factors of production can be varied and even the state of technology is able to change. (Supply is perfectly elastic)

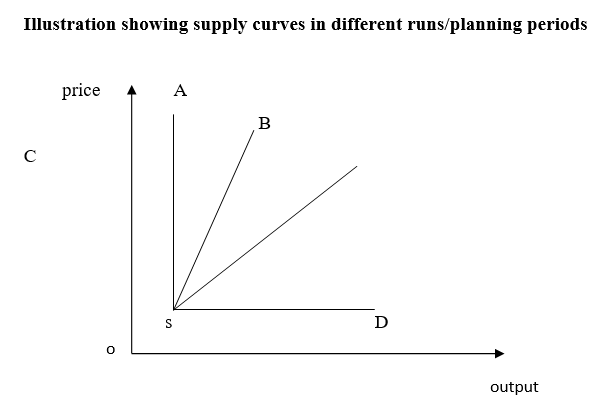

Where the supply curves are:

A is very short run

B is short run

C is long run

D is very long run

Production function

Production function refers to the technical relationship between the level of output produced and the amount of inputs used in production at a particular time with a given state of technology.

Q=f (inputs)

Q=f(x1, x2, x3, x4……xn)

Where:

Q=quantity of output

X=different inputs.

Factors determining the production function

- the level of technology

- the size of the firm

- quality and quantity of inputs

- degree of a firm’s organization

- the cost of factors of production

- political climate